Introduction

- The Department for Communities (the Department) is responsible for housing, urban regeneration, community development, social security and child maintenance. The annual budget for the Department is £8.4 billion, of which approximately £7.1 billion is spent on benefits.

- The Department administers £6.6 billion of benefits directly with a further £0.5 billion of housing benefits administered by the Northern Ireland Housing Executive (the Housing Executive) and Land and Property Services (LPS).

- This Report reviews the results of my 2021-22 audit of the Department’s accounts and sets out:

- the reasons and context for my qualified regularity audit opinion in relation to the material level of estimated fraud and error in benefit expenditure;

- a high level comparison of fraud and error rates with Great Britain; and

- progress on Housing Association inspections.

Key findings

Estimated Fraud and error in benefit expenditure

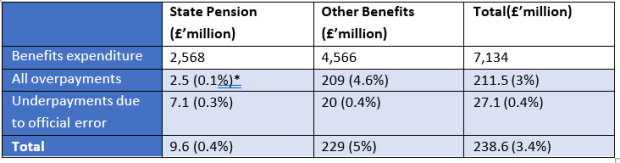

- I have qualified my opinion on the regularity of the Department’s financial statements due to the material level of estimated fraud and error in benefit expenditure. I exclude State Pension from my qualified opinion because the estimated level of fraud and error in this benefit is much lower than in other benefits, being £9.6 million in expenditure of £2.6 billion (see Figure 1).

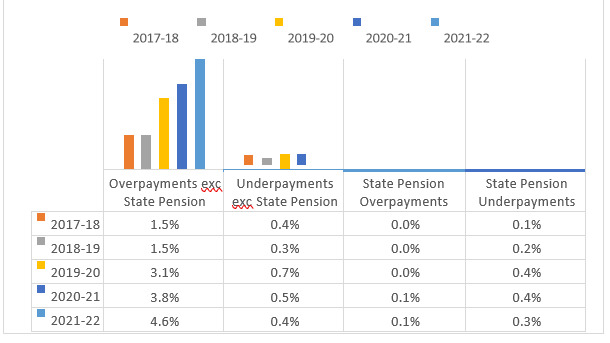

- Estimated overpayment and underpayment rates for benefits now stand at 4.6 and 0.4 per cent respectively of benefit expenditure, excluding State Pension, and are at the highest rate for several years (see Figure 2). In terms of value this represents £209 million in overpayments and £20 million in underpayments. Of this overpayments figure, 60 per cent (£124 million) relates to overpayments arising from Universal Credit.

- The level of estimated fraud and error in housing benefit expenditure, included in the Department’s financial statements, is material and forms part of my qualification. As this

benefit is paid to claimants out of the Housing Executive accounts and the LPS Statement of Rate Levy Account, I also qualify my regularity audit opinion on these accounts in respect of the level of estimated fraud and error in housing benefit expenditure.

Progress in Housing Association inspections

- Last year I raised concerns about the gap in assurances available to the Accounting Officer in the absence of a regular programme of Social Housing Development Programme inspections. These inspections provide the Accounting Officer with assurance over how the Housing Association Grant is used and how Registered Housing Associations’ (RHAs) comply with both the Housing Association Guide and NI Public Procurement Policy. I welcome the considerable progress the Department has been making towards resuming a full programme of inspections.

- As part of its regulatory role the Department is required to assess all RHAs annually against set standards. Since 2017 this requirement has been met for all RHAs except for Woodvale and Shankill Community Housing Association due to an ongoing Judicial Review raised against the Department. I accept that the Department continues to follow legal advice but am concerned that this Association did not have adequate Department scrutiny for a number of years. I note that, following recent legal advice, annual assessment within this Association has now re- commenced.

Qualification of the Comptroller and Auditor General’s audit opinion on the regularity of benefit expenditure (excluding State Pension)

- I have qualified my opinion on the regularity of the Department’s financial statements due to the material level of estimated fraud and error in benefit expenditure, except for expenditure on State Pension where the estimate is significantly lower.

- I am required under the Government Resources and Accounts Act (Northern Ireland) 2001 to report my opinion as to whether the financial statements give a true and fair view. I am also required to report my opinion on regularity, that is, whether in all material respects the expenditure and income have been applied to the purposes intended by the Northern Ireland Assembly and the financial transactions conform to the authorities that govern them.

- Legislation specifies the entitlement criteria for each benefit, and the method to be used to calculate the amount to be paid. Where fraud or error results in the payment of a benefit to an individual who is not entitled to that benefit; or a benefit is paid at a rate that differs from the amount specified in legislation, the over or under payment does not conform to the Assembly’s intention and is irregular.

- In my opinion, the estimated value of overpayments and underpayments due to fraud and error in benefits, other than State Pension, remains material and the qualification of my audit opinion reflects this. The Department’s accounts have been qualified for a number of years due to material levels of overpayments and underpayments in benefit expenditure. The nature and reasons for these levels of fraud and error vary every year.

Measuring fraud and error

- Benefit payments are susceptible to intentional error by claimants (customer fraud) and, also to unintended error by claimants (customer error) and the Department (official error). The Department is reliant on claimants’ accurate and timely notification of changes of circumstances and the complexity of benefits can cause confusion and genuine error, especially for those with means-tested entitlements.

- The Department selects random samples from the total benefit caseload to test their financial accuracy and provide a measure of official error, and conducts benefit reviews that provide a measure of customer fraud and error. The Department estimates total fraud and error, set out in Note 23 to the accounts, by combining the results from these reviews. The fraud and error figures that are quoted are statistically determined central estimates (or mid-points) within a range. I am satisfied that the scope of this range is not material. We have reviewed and tested the Departments’ methodology for estimating fraud and error.

- In order to facilitate the timetable for the production of the accounts, the Department’s testing of financial accuracy is reported on a rolling 12 month basis, not on a financial year basis. I am satisfied that this approach is reasonable and that the results produced are a reliable estimate of the total fraud and error in the benefits’ system.

- Note 23 to the Accounts sets out which benefits were measured for financial accuracy and subject to benefit review this year. The level of fraud and error for the remaining benefits has been estimated using either the results of previous financial accuracy or benefit review exercises or by proxy values.

- Benefit reviews, which estimate customer fraud and error, for both Disability Living Allowance (DLA) and State Pension have not been completed since 2008 and 2009 respectively. I acknowledge that DLA for working-age claimants is continuing to reduce as it is replaced by Personal Independence Payment and that the 2009 State Pension estimates for customer error and fraud were fairly low at 0.2 per cent and zero per cent respectively. However, the absence of complete up-to-date information on fraud and error rates in large benefits creates a risk that the Department is not targeting its activities to reduce fraud and error effectively.

- The need for regular review has been illustrated following a number of pensioners contacting the Department for Work and Pension (DWP) in January 2020 to confirm the accuracy of their State Pension. In August 2020 DWP confirmed there was a significant issue and estimated that it had underpaid 134,000 pensioners over £1 billion, an average of £8,900 each. DWP’s review of all possibly affected cases is ongoing and since July 2020 the Department has been working with it to identify claimants, potentially underpaid in Northern Ireland. So far nearly 5,000 cases have been reviewed and £4.6 million in arrears has been paid out to NI claimants.

- In January 2022 the Westminster Public Accounts Committee (PAC) concluded that DWP had been relying on a State Pension payment system that is not fit for purpose. The Committee noted that DWP’s assurance attention was focused elsewhere due to low annual error rates on State Pension and that there was a risk that similar, unidentified errors exist elsewhere in the State Pension caseload. The Committee made seven recommendations which included the need to consider if there are costs effective ways to upgrade State Pension IT systems, enhance administrative processes and improve the clarity and availability of information to claimants and the next of kin of deceased claimants.

- I accept that the Department is reliant on DWP’s IT systems for processing benefit expenditure and that the Department intends to fully measure State Pension in its 2022 programme. While this is welcome, given the fact that the Department was apprised of this issue in March 2020, I am disappointed that it did not act with pace and include the review of State Pension in its 2021 programme.

- It is reassuring that DWP’s full review of State Pension in 2021 showed that estimated overpayment rates continue to be low. However this benefits review exercise identified a further issue in respect of state pensions being underpaid to certain claimants. It is hoped that the Department’s full review of State Pension next year will provide similar assurance over overpayment rates in NI and help the Department better assess the impact of these state pension underpayments issues for NI claimants.

- I am satisfied that the use of previous sampling exercises and proxy values is a reasonable measure of the level of estimated fraud and error in unmeasured benefits.

The estimated level of fraud and error in benefit expenditure

- Fraud and error levels in State Pension benefit expenditure of £2.6 billion (2020-21: £2.4 billion) remain at an immaterial level, estimated at 0.4 per cent of expenditure for both over and underpayments (see Figure 1). As a result, I continue to exclude State Pension expenditure from my qualified opinion on the accounts.

Figure 1: Estimated total overpayments and underpayments due to official error in benefit expenditure due to fraud and error

*Percentage of benefits expenditure

- Figure 2 shows the overpayment and underpayment rates as a percentage of benefit expenditure since 2017-18. The overpayment rate has tripled since then and is at its highest level to date. I note that the significant increase in overpayments this year is largely attributable to increasing customer fraud which has gone up from £99.5 million (1.5 per cent) to £138 million (1.9 per cent).

- The Department considers that the increase in customer fraud this year is mainly due to the significant increase in Universal Credit (UC) fraud which has doubled in value again this year to

£101.7 million (2020-21: £51.8 million) with the overpayment rate increasing from 7.2 per cent to 11.2 per cent. Universal Credit was fully measured for the last two years and movements in overpayment and underpayment rates for estimated fraud and error are set out in Figure 3:

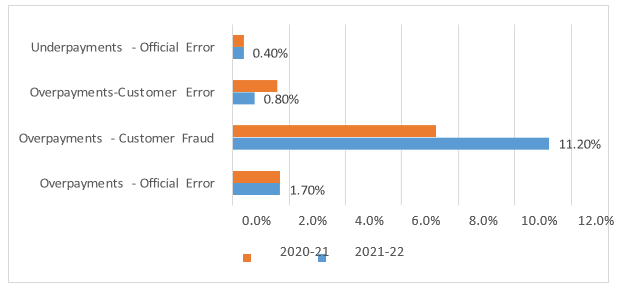

Figure 3: Change in estimated overpayment and underpayment rates for Universal Credit

- Expenditure on UC increased by 27 percent from £716 million in 2020-21 to £912 million this year and accounts for nearly 13 per cent of overall benefit expenditure. The Department’s analysis of UC fraud cases shows that:

- 28 per cent of the cases commenced during the early days of the pandemic when checks to new claims were paused to manage the surge in demand and restrictions in place; and

- a significant proportion relate to self-employed income which is more difficult to verify than taxed income through HMRC records.

- I note that the GB position with respect to UC is similar in terms of increasing expenditure and estimated overpayment rates due to customer fraud of 13 per cent. However I am concerned that estimated overpayments due to fraud of 11.2 per cent (£101.7 million) in NI are so significant, particularly given its size, and consider this to be unacceptable. Moreover this will potentially increase when the Department starts transferring claimants from legacy benefits to UC (managed migration).

- The Department has highlighted a number of initiatives to reduce fraud and error in social security benefits, including UC, in Note 23 and I asked what its strategy is for reducing UC fraud and error and what the barriers are in achieving this. The Department told me that it continues to enhance its understanding of the root causes of fraud and error within the benefit system and has targeted plans in place to minimise loss to the public purse, tackling those areas of highest risk. The Department’s Benefit Fraud, Error and Debt Strategy sets out high-level objectives of preventing fraud and error from occurring or detecting it as early as possible during the life of a claim. The Department’s Benefit Security Division takes the lead in driving activity to minimise fraud and error and undertakes a range of counter fraud activities from targeted interventions to criminal investigations for the most serious frauds. This complements the risk based targeted work carried out by individual benefit branches.

- Furthermore as a digital benefit with 24/7 access the fraud and error picture within UC remains challenging and is influenced by a number of factors for example, customer behaviour, both opportunistic and organised activity. There has been significant and ongoing development of the UC system along with future exploration of additional measures that can be taken to reduce both fraud and error. These include ongoing investment in enhanced checking activity throughout the claim journey. Close engagement with DWP continues to ensure the Department is fully sighted on the longer term strategy for Universal Credit fraud & error.

Estimated fraud and error in Northern Ireland and Great Britain – high level comparison

- Looking at comparable figures in GB, including State Pension, overpayment error rates have increased from 3.9 per cent in 2020-21 to 4 per cent this year. In Northern Ireland, the corresponding overpayment error rate has increased from 2.5 per cent to 3 per cent. Underpayment rates for official error have reduced from 0.5 per cent to 0.4 per cent in Northern Ireland, lower than GB’s rate of 0.5 per cent.

Progress in Housing Association inspections

- The Department is responsible for the funding, monitoring, regulation and issue of guidance and policy directives to Registered Housing Associations. There are 20 Registered Housing Associations (RHAs) in Northern Ireland. The Department carries out two different types of inspection:

-

- as part of its regulatory role the Department is required to assess the performance of every RHA annually against governance, finance and consumer standards; and

- to provide assurance to the Accounting Officer over spend on the Social Housing Development Programme (SHDP) the Department inspects a sample of individual schemes or adaptations.

Regulatory Assessments

- Since 2017 annual regulatory assessments have been completed for all of the RHAs, except Woodvale and Shankill Community Housing Association (WSCHA), following legal advice in respect of the matters referred to in the next paragraph. WSCHA provides for upgrades and maintains general family housing needs, sheltered accommodation for the elderly and disabled and special needs accommodation. It is responsible for managing approximately 460 units and has been registered with the Charities Commission since March 2015.

- Following a number of whistleblower allegations in 2016 the Department commissioned a Governance Review of the specific matters raised in respect of WSCHA. After the review was completed in 2017, a Statutory Inquiry (SI) was launched into the affairs of WSCHA. The results of this SI have not been published as WSCHA subsequently raised a Judicial Review (JR) against the Department on a separate issue. This JR remains ongoing and the Department continues to seek legal advice. The Charities Commission NI launched their own SI into WSCHA in January 2020 which has recently concluded.

- It is concerning that this RHA has been operating without adequate Department scrutiny in the past five years but I welcome the fact that, following further legal advice, a regulatory assessment is underway for 2020-21. My staff intend to monitor the position with respect to this RHA closely.

Social Housing Development Programme (SHDP) inspections

- The Department provided funding of £172 million (2020-21: £136 million) via the Housing Executive to Registered Housing Associations (RHAs) during 2021-22 for the delivery of social

housing through the SHDP.

- In 2019 the Department’s Internal Audit Unit reported that SHDP inspections had not taken place since April 2016. The purpose of these inspections is to ensure that RHAs have complied with the Housing Association Guide and NI Procurement policy and therefore they provide the Accounting Officer with assurance over how SHDP money has been spent. Last year I expressed my concern about the limited progress that had been made in re-instating a programme of inspections. The Department introduced a three year plan from 2020-21 to 2022-23 to cover the 13 RHAs who continue to develop schemes and this year completed 20 desk-based inspections in which no major issues were identified except for one inspection where the Department identified significant procurement issues and planning conditions not being fully met. The Department is following these issues up with the Association. While the target of 31 inspections has not been achieved this year, I note that 11 further reports are either at fieldwork or draft stage and schemes and adaptations in 10 of the 13 developing RHAs have been inspected to date.

- I welcome the considerable progress the Department is making in this area which should provide greater assurance to the Accounting Officer over how this money is spent. Due to the historic issues around inspections in the SHDP my staff will keep this matter under review.

KJ Donnelly

Comptroller and Auditor General Northern Ireland Audit Office

1 Bradford Court Galwally BELFAST

BT8 6RB

July 2022