Introduction

- The Department for Communities (the Department) is responsible for housing, urban regeneration, community development, social security and child support. The annual budget for the Department is £8.5 billion, of which approximately £7.2 billion is spent on benefits.

- The Department administers £6.2 billion1 of benefits directly with a further £0.6 billion of housing benefits administered by the Northern Ireland Housing Executive (the Housing Executive) and Land and Property Services (LPS).

- This Report reviews the results of my 2020-21 audit of the Department’s accounts and sets out:

- the reasons and context for my qualified regularity audit opinion in relation to the material level of estimated fraud and error in benefit expenditure;

- a high level comparison of fraud and error rates with Great Britain;

- impact of the COVID-19 pandemic; and

- the gap in assurances available to the Accounting Officer over the Social Housing Development Programme.

Key findings

Estimated Fraud and error in benefit expenditure

- I have qualified my opinion on the regularity of the Department’s financial statements due to the material level of fraud and error in benefit expenditure. I exclude State Pension from my qualified opinion because the estimated level of error is much lower than in other benefits (£11.9 million in expenditure of £2.5 billion, see Figure 1).

- Overpayments of benefits due to fraud and error, continue to increase and are now at their highest estimated rate for several years. The estimated overpayment and underpayment rate for benefits now stands at 3.8 and 0.5 per cent of the £4.4 billion of expenditure on benefits for 2020-21 respectively, excluding State Pension. This comprises overpayments of £166.3 million and underpayments of £23.8 million (see Figure 1). Of this overpayments figure, £75.4 million relates to Universal Credit.

- The level of estimated fraud and error in housing benefit expenditure, included in the Department’s financial statements, is material and forms part of my qualification. As this

benefit is paid to claimants out of the Housing Executive accounts and the LPS Statement of Rate Levy Account, I also qualify my regularity audit opinion on these accounts in respect of housing benefit expenditure.

1 These figures are from Note 23 to the accounts as the Department measures the level of estimated fraud and error in benefit expenditure on a calendar year basis. The financial statements disclose overall benefit expenditure for 2020-21 of approximately £7.2 billion, on a financial year basis.

Impact of the COVID-19 pandemic

- There was a significant increase in Universal Credit claims during the year with expenditure increasing by 140 per cent and new claims peaking at 34,500 in March 2020 as compared to a monthly average of 7,000. To meet this increased demand and provide support to those in urgent need the Department implemented temporary policy changes and redeployed staff from other areas.

- The NI Executive allocated the Department an additional £271 million in funding this year and the Department spent £26 million of its normal allocated funding to mitigate against the COVID-19 pandemic (see paragraph 30). Additional funding was provided at national level for the increase in both Universal Credit and Jobseekers’ Allowance claims. My staff have looked at a number of the COVID-19 schemes and found that payments were made in line with the rules of the scheme. I have not, however, assessed whether value for money has been achieved. I reported separately2 on the £25 million allocated to the Sports Sustainability Fund (which falls within the Sports Hardship Fund of £27 million).

Gaps in assurance over the Social Housing Development Programme (SHDP)

- As the Department has not been carrying out a full programme of SHDP inspections since April 2016, we consider that there is a gap in assurances available to the Accounting Officer. These inspections provide the Accounting Officer with assurance over how the Housing Association Grant is used and Registered Housing Associations’ (RHAs) compliance with both the Housing Association Guide and NI Public Procurement Policy. The Department has now restarted its programme of inspections although the numbers were limited in 2020-21 because of the impact of the COVID-19 pandemic. We expect a full programme of inspections to be fulfilled next year.

Qualification of the Comptroller and Auditor General’s audit opinion on the regularity of benefit expenditure (excluding State Pension)

- I have qualified my opinion on the regularity of the Department’s financial statements due to the material level of estimated fraud and error in benefit expenditure except for expenditure on State Pension where the estimate is significantly lower.

- I am required under the Government Resources and Accounts Act (Northern Ireland) 2001 to report my opinion as to whether the financial statements give a true and fair view. I am also required to report my opinion on regularity, that is, whether in all material respects the expenditure and income have been applied to the purposes intended by the Northern Ireland Assembly and the financial transactions conform to the authorities that govern them.

- Legislation specifies the entitlement criteria for each benefit, and the method to be used to calculate the amount to be paid. Where fraud or error results in the payment of a benefit to

2 Sports Sustainability Fund Report, Report by the Comptroller and Auditor General, 22 June 2021.

an individual who is not entitled to that benefit; or a benefit is paid at a rate that differs from the amount specified in legislation, the over or under payment3 does not conform to the

Assembly’s intention and is irregular.

- In my opinion, the estimated value of overpayments and underpayments due to fraud and error in benefits, other than State Pension, remains material and the qualification of my audit opinion reflects this. The Department’s accounts have been qualified for a number of years due to material levels of overpayments and underpayments in benefit expenditure. The nature and reasons for these levels of fraud and error vary every year.

Measuring fraud and error

- Benefit payments are susceptible to intentional error by claimants (customer fraud) and, also to unintended error by claimants (customer error) and the Department (official error). The Department is reliant on claimants’ accurate and timely notification of changes of circumstances and the complexity of benefits can cause confusion and genuine error, especially for those with means-tested entitlements.

- The Department selects random samples from the total benefit caseload to test their financial accuracy and provide a measure of official error, and conducts benefit reviews that provide a measure of customer fraud and error. The Department estimates total fraud and error, set out in Note 23 to the accounts, by combining the results from these reviews. The fraud and error figures that are quoted are statistically determined central estimates (or mid-points) within a range. While this range is higher than usual this year4, due to additional uncertainties arising from introducing previous years’ data, I am satisfied that the scope of this range is not material.

- In order to facilitate the timetable for the production of the accounts, the Department’s testing of financial accuracy is reported on a rolling 12 month basis, not on a financial year basis. I am satisfied that this approach is reasonable and that the results produced are a

reliable estimate of the total fraud and error in the benefits’ system.

- Benefit reviews, which estimate customer fraud and error, for both Disability Living Allowance (DLA) and State Pension have not been completed since 2008 and 2009 respectively. I acknowledge that DLA for working-age claimants is continuing to reduce as it is replaced by Personal Independence Payment and that the 2009 State Pension estimates for customer error and fraud were fairly low at 0.2 per cent and zero per cent respectively. The absence of complete up-to-date information on fraud and error rates in large benefits creates a risk that the Department is not targeting its activities to reduce fraud and error effectively. I note that DWP is planning a full review of State Pension next year and the Department is considering this as part of their work programme for the year after.

3 Only underpayments due to official error are considered to be irregular.

4 The Department is 95% sure that the total overpayments’ estimate lies within the range £133 million (2 per cent) to £209 million (3.1 per cent). The Department is 95% sure that the total underpayments estimate lies within the range £38 million (0.6 per cent) to £82 million (1.2 per cent).

- As I reported last year, the Department was unable to complete its full measurement programme this year due to the impact of the COVID-19 pandemic. A full fraud and error review was completed for Universal Credit, considered to have the highest risk and official error was measured for State Pension, which has the highest spend. The Department also measured the level of official error within Housing Benefit expenditure. The level of fraud and error for the remaining benefits has been estimated using either the results of previous financial accuracy or benefit review exercises or by proxy values5.

- It is recognised that, due to the increase in volume of claims, less experienced staff and the reduction in usual controls6, there is likely to be a higher level of fraud and error this year. Basing estimated fraud and error for this year on previous sampling exercises or proxy values for unmeasured benefits may not fully reflect this. DWP assessed the validity of using these methods and concluded that an adjustment was not required due to potential impacts of benefit easements related to the pandemic. Following an analysis of trends in estimated levels of fraud and error, the Department is content that DWP’s approach is also applicable to Northern Ireland.

- I am satisfied that the use of previous sampling exercises and proxy values is a reasonable measure of the level of estimated fraud and error in unmeasured benefits.

The estimated level of fraud and error in benefit expenditure

- Fraud and error levels in State Pension benefit expenditure of £2.5 billion (2019-20: £2.4 billion) remain at an immaterial level, estimated at 0.5 per cent of expenditure for both over and underpayments (see Figure 1). As a result, I continue to exclude State Pension expenditure from my qualified opinion on the accounts. The estimated rate of overpayments has increased again to 3.8 per cent (£166.3 million) from 3.1 per cent (£124 million) in 2019-

20. The estimated rate of underpayments, excluding State Pension, has decreased to 0.5 per cent (£23.8 million) from its estimated rate of 0.7 per cent (£26 million) in 2019-20.

Figure 1: Estimated total overpayments and underpayments due to official error in benefit expenditure due to fraud and error

|

|

State Pension (£’million) |

Other Benefits (£’million) |

Total (£’million) |

|

Benefits expenditure |

2,457 |

4,362 |

6,819 |

|

All Overpayments |

1.5 (0.1%) |

166.3 (3.8%) |

167.8 (2.5%) |

|

Underpayments due to official error |

10.4 (0.4%) |

23.8 (0.5%) |

34.2 (0.5%) |

|

Total |

11.9 (0.5%) |

190.1 (4.3%) |

202 (3%) |

Source: Department for Communities Resource Account 2020-21.

5 The level of fraud and error for benefits that have not been measured during the year is either estimated from the results of previous sampling exercises (financial accuracy or benefit reviews) or based on a proxy values then rolled forward. A proxy value used for unmeasured benefits is closely related to a measured benefit in terms of claimant entitlement characteristics, for example, Disability Living Allowance is used as a proxy measure for fraud and error in Attendance Allowance.

6 For example, suspension of face-to-face interviews, automatic extension of awards instead of reviewing them and a reduction in checks on claimant information.

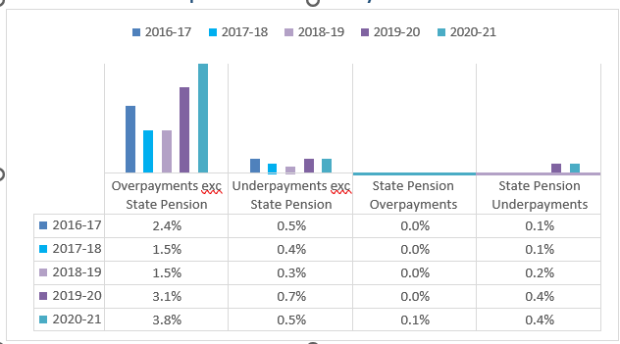

- Figure 2 shows the overpayment and underpayment rates as a percentage of benefit expenditure since 2016-17. The overpayment rate has more than doubled since 2018-19 and is at its highest level to date. I note that the significant increase in overpayments this year is largely attributable to increasing customer fraud which has gone up from 1 per cent (£65 million) to 1.5 per cent (£99.5 million), with a slight improvement in the level of official error and a small increase in customer error. The Department considers that the increase in customer fraud this year is due to an increase in Universal Credit fraud. It told me that:

- at the beginning of the coronavirus pandemic, there was a sudden surge in claims for Universal Credit with new claims peaking at ten times the usual volumes for a number of weeks. The number of adults claiming Universal Credit rose incrementally over 36 months to reach 70,000 in early March 2020 but due to the pandemic increased substantially in just 2 months to 134,000 by the end of May 2020; and

- there was an increase in the proportion of high risk claims within the caseload. To get money as quickly as possible to those who needed it a number of operational easements and changes to benefit administration were introduced for a short time in both Great Britain and Northern Ireland which included changes to the verification processes, placing a reliance on a claimant’s declaration of their circumstances. This approach was necessary to manage the need to make payments on time to vulnerable customers following the sudden surge of claims during an emergency situation.

Figure 2: Trends in over and underpayments due to estimated fraud and error as a percentage of relevant benefit expenditure for the last 5 years

Source: Department for Communities Resource Account 2016-17 - 2020-21.

- The only benefit that has been fully measured this year is Universal Credit. While the overall estimated value of overpayments of £75.4 million is more than double the prior year figure of

£31 million the overpayment error rate of 10.5 per cent is broadly the same. Movements in overpayment and underpayment rates for estimated fraud and error rates since 2019-20 are set out in Figure 3:

Figure 3: Change in estimated overpayment and underpayment rates for Universal Credit

Source: Department for Communities Resource Account 2019-20- 2020-21.

- While the estimated rates of overpayments due to official error in Universal Credit have decreased this year from 5 per cent to 1.7 per cent, the corresponding rates due to customer fraud have increased from 5.2 per cent to 7.2 per cent. I welcome the reduction in official error rates this year particularly given the complexity of this benefit.

Comparisons between Northern Ireland and Great Britain – high level comparison

- We have reviewed and tested the Departments’ methodology for estimating fraud and error. Looking at comparable figures in GB7, including State Pension, overpayment error rates have increased significantly from 2.4 per cent in 2019-20 to 3.9 per cent this year. In Northern Ireland, the corresponding overpayment error rate has increased from 2 per cent to 2.5 per cent. Underpayment rates for official error have reduced from 0.6 per cent to 0.5 per cent in Northern Ireland, slightly higher than GB’s rate of 0.4 per cent.

The impact of the COVID-19 pandemic on UC

- As noted earlier there was a significant increase in Universal Credit claims this year due to the COVID-19 pandemic. At the end of February 2020 there were nearly 58,000 households on Universal Credit. By the end of February 2021 this had increased to just over 118,000. Consequently this year, expenditure on Universal Credit increased from £295 million to £716 million8 (an increase of 140 per cent).

- The Department told me that frontline staff identified 3,500 suspicious claims, of which 60 per cent were found to be wholly or partially suspicious. Wholly suspicious claims (52 per cent) were not paid nor was the suspicious element, for example, housing costs. It is encouraging that in the midst of the pressures arising from the pandemic that Department staff were alert to the possibility of fraud and acted accordingly.

7 Fraud and Error in the benefit system for financial year ending 2021, 13 May 2021, DWP National Statistics. The benefit expenditure figures exclude amounts devolved to the Scottish Government of £3.2 billion.

8 On a calendar year basis. On a financial year basis it increased from £362 million to £831 million (130 per cent increase).

The impact of the COVID-19 pandemic on benefits and other expenditure

- By the end of February 2021, the Westminster Government provided estimated additional funding of £277 million and £4.7 million to cover the costs of additional Universal Credit and Jobseekers’ Allowance claims9.

- The Department was also allocated £271 million in funding this year by the Northern Ireland Executive to deliver various schemes to mitigate against the worst effects of COVID-199. Figure 4 shows the breakdown of this funding.

Figure 4: Funding allocated to the Department for COVID-19 during 2020-21

|

COVID-19 Scheme |

Funding (£’000) |

|

Grants to Local Councils |

85,300 |

|

Heating Payment |

44,200 |

|

Sports Hardship Fund |

27,000 |

|

Culture Resilience Scheme (Culture Recovery) |

23,300 |

|

Culture Resilience Fund |

4,000 |

|

Charitable Grants |

20,500 |

|

Access to Food Packages |

13,500 |

|

Supporting People |

8,400 |

|

Community Support Fund |

9,500 |

|

Social Enterprise Support |

9,300 |

|

Homelessness |

7,100 |

|

Benefit Delivery Response |

5,000 |

|

Loss of Rental Income (NI Housing Executive Landlord) |

4,500 |

|

Discretionary Support |

3,000 |

|

Community, Voluntary and Social Enterprise Sector (Personal Protective Equipment) |

2,500 |

|

NI Housing Executive Supplier Payments Relief |

1,600 |

|

Department of Health Jointly Supported Living Scheme Care Costs |

1,200 |

|

NI Housing Executive Supporting People (Personal Protective Equipment) |

1,100 |

|

TOTAL |

271,000 |

Source: Department for Communities

- In addition, the Department spent £26 million of its own allocated funding to help mitigate the impact of the COVID-19 pandemic with £12 million being spent on a COVID-19 revitalisation programme, delivered in partnership with Councils, and approximately £6 million on IT equipment for staff to enable working from home.

9 Second Report-Overview of the Northern Ireland Executive’s Response to the COVID-19 Pandemic, Report by the Comptroller and Auditor General, 8 June 2021. The figures in this Report are based on estimates and reflect expenditure to date.

- The Department had to make these payments within a very short timeframe and therefore it may be possible that controls over this expenditure were not as robust as they would have been normally. While my staff have looked at a number of these schemes and found that they were paid in line with the rules of the scheme I have not assessed whether value for money has been achieved.

- As noted in paragraph 8, I reported separately on the £25 million allocated to Sports Sustainability Fund (which falls within the Sports Hardship Fund of £27 million) in June 2021.

Gaps in assurance over the Social Housing Development Programme (SHDP)

- The Department provided funding of £136 million via the Housing Executive to Registered Housing Associations (RHAs) during 2020-21 for the delivery of new social housing through the SHDP10. The Department carries out a rolling programme of individual SHDP inspections to provide the Accounting Officer with assurance over the use of the Housing Association Grant and ensure that RHAs comply with both the Guide and NI Public Procurement Policy.

- In 2019 the Department’s Internal Audit Unit reported that SHDP inspections had not taken place since April 2016. The Department instigated a pilot exercise in 2019-20 but due to COVID-19 restrictions, only two inspections were completed and five inspections (£1.6 million) have been completed in 2020-21.

- In previous years I have reported extensively on the area of Housing Association inspections, most recently in June 201611. It is disappointing that the Department has been unable to complete a full inspection programme for a number of years. While I appreciate the many challenges the Department is facing in terms of resourcing and additional COVID-19 pressures, until a full programme of inspections is completed there continues to be reduced assurance available to the Accounting Officer over the SHDP. I intend to monitor this situation closely.

KJ Donnelly

Comptroller and Auditor General Northern Ireland Audit Office

1 Bradford Court Galwally BELFAST

BT8 6RB

August 2021